Trailer orders leapt forward in November, with FTR reporting orders up 42% month over month and ACT Research stating an increase of about 4,000 units.

FTR says its preliminary order total was 22,745 units, which is the highest net order since December 2023 and ends a streak of weak months for trailer orders. ACT's estimate was slightly under at 20,500 units, down 4% year over year. The company adds its seasonal adjustment (SA) at this point in the annual order cycle lowers November’s tally to 15,000 units, but that’s about 22% above October’s seasonally adjusted intake.

[RELATED: FTR peers into future with record inventory and a new administration]

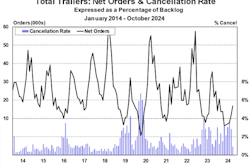

“Since we’re still in the early stages of the traditional start to the order season, this month’s uptick was expected. It’s also no surprise that the data is below the November 2023 intake, given the softer demand recorded throughout this year,” says Jennifer McNealy, director, CV market research and publications at ACT Research. “That said, and with the caution that one data point does not make a trend, perhaps November data are bearing witness to the anecdotal information about increased quotation activity that we have been hearing the past few months. However, as illustrated in the attached graph, this is typical year-end order behavior, so the stickiness of November’s ‘trend’ will be determined as more data arrive in the coming months.”

However, FTR says total trailer net orders for 2025 look sluggish, down the same amount — 42% year over year. Headwinds come from a sluggish freight market, FTR says, driving November's trailer build down to 13,238 units, or 43% year over year. It's the lowest monthly production level since 2010.

"As we have discussed in the context of Class 8 truck orders, President-elect Trump's plan to impose immediate tariffs on imports from Mexico, Canada and China will add to the challenges," says Dan Moyer, senior analyst for commercial vehicles. "Those tariffs would significantly raise costs for fully assembled trailers imported from Mexico and Canada as well as for critical automotive parts sourced from these regions and China that are essential to U.S.-based trailer production. Resulting supply chain disruptions and/or cost increases could mean higher trailer prices, altered trade cycles and buyer demand patterns, and strains on fleet operator budgets. Slightly elevated dealer inventories might temporarily meet a short-term demand surge as buyers attempt to avoid higher costs, but the potential for increased costs for Class 8 tractors might prompt some fleets to continue prioritizing purchasing power units over trailers in the near term."

[RELATED: Trailer cancelations down in October]

Net orders in November were above total production, FTR says, increasing backlogs by 10,124 units (up 12% month over month) to 92,213 units. Lower month-over-month production and growing backlogs pushed the backlog/build ratio up to seven months, the highest reading since February. This indicates some decreasing pressure on OEMs to scale back production in the near term, FTR says.

The commercial vehicle market continued to see a disconnect between the demand for trailers and the demand for trucks, FTR notes. North American Class 8 net orders increased 2% year over year in September and November. U.S. trailer net orders dropped by 42% year over year during the same period. For-hire fleets have been prioritizing investments in new power units over trailers this year, FTR says, likely influenced by reduced profitability or shifts in trade cycles.

OEMs have cut back on production, but if 2025 trailer orders remain down, some OEMs may need to extend or deepen production cuts.

“Despite the order improvement, ACT’s expectations for weak trailer demand relative to recent performance remain, as continuing weak for-hire truck market fundamentals, low used equipment valuations, relatively full dealer inventories, and high interest rates impede stronger activity, especially into early 2025. An order uptick showcasing demand, or the lack thereof, depends not just on the first few months of the new order cycle, but at least on order volumes through the first quarter of 2025,” McNealy says.